Saving vs investing — when to choose which in 2025 is one of the most important financial decisions individuals and families must make this year. With inflation still influencing purchasing power, interest rates shifting, and AI-powered financial tools becoming the norm, knowing when to save and when to invest can dramatically affect your wealth and stability.

This comprehensive guide breaks down both options, explains when each is appropriate, and provides expert-backed recommendations tailored for 2025’s financial landscape.

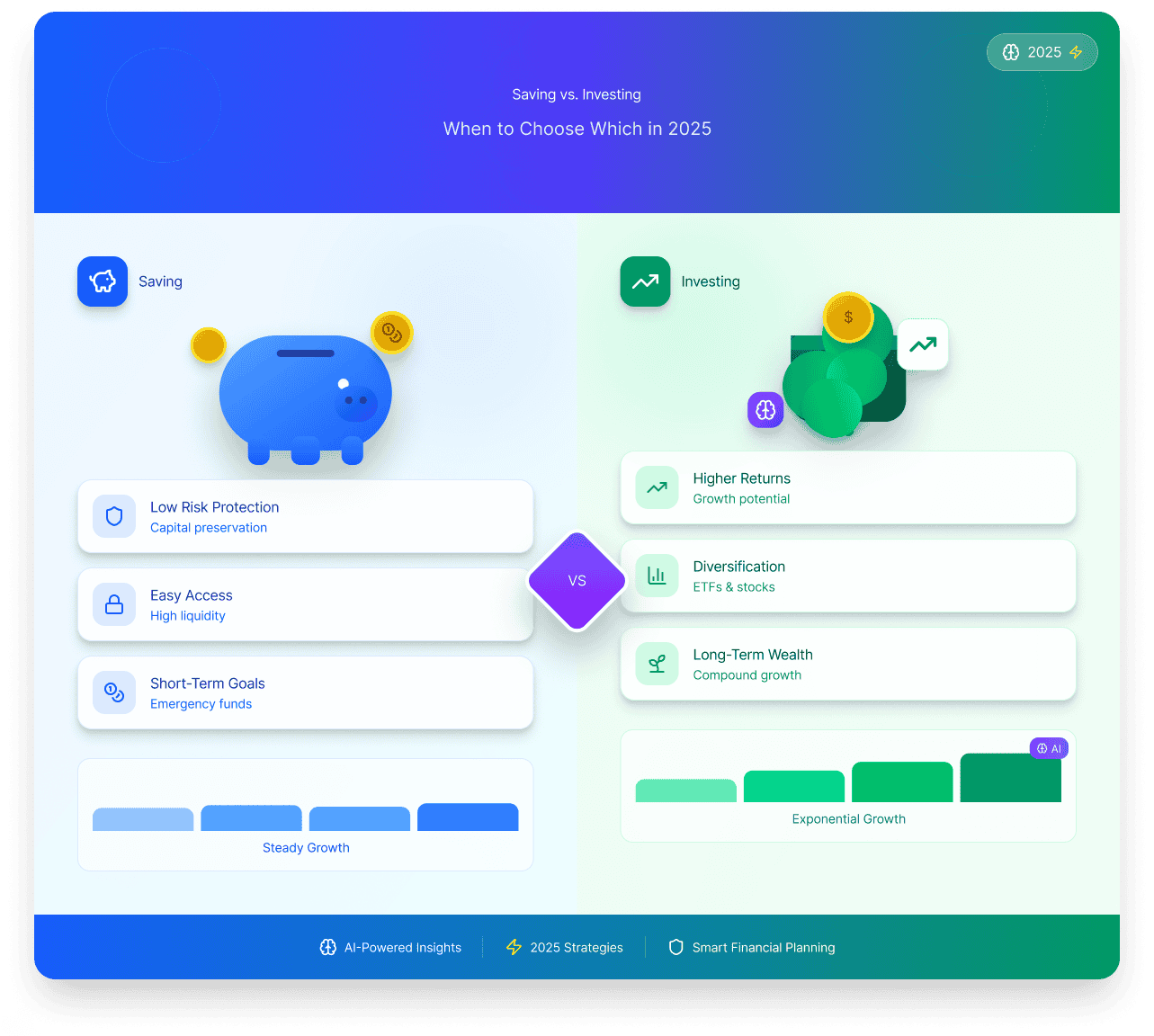

What saving means in 2025

Saving in 2025 refers to setting aside money in low-risk, highly liquid accounts such as:

- High-yield savings accounts

- Money market accounts

- Certificates of deposit (CDs)

- Digital wallets with saving features (Apple Card Savings, Revolut Vaults, etc.)

Key 2025 trends influencing saving

- Higher baseline interest rates compared to the early 2020s

- AI-driven savings automations that adjust contributions based on spending

- Increased emergency fund awareness due to global uncertainty

- Fintech apps offering real-time goals tracking

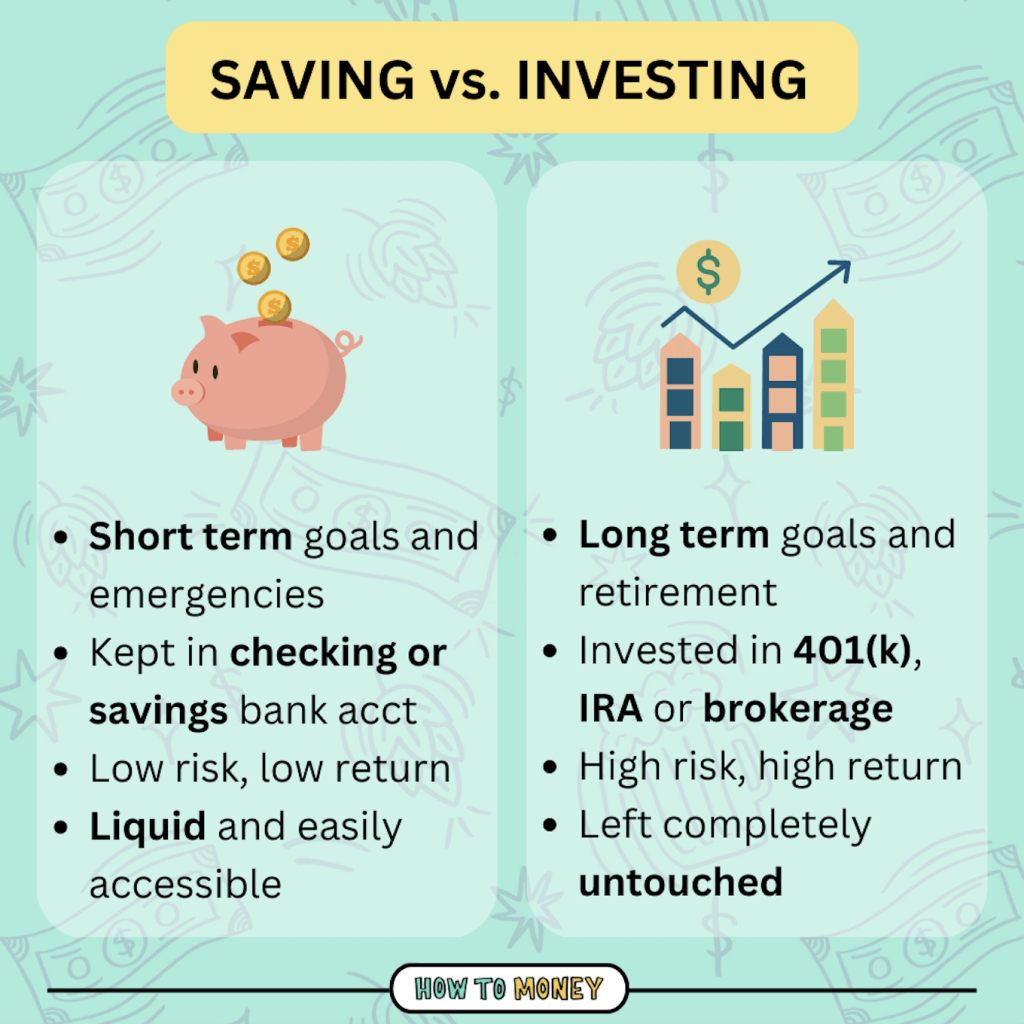

Benefits of saving

- Guaranteed returns (FDIC/NCUA insured)

- Immediate access to cash

- Zero volatility

- Ideal for short-term goals (0–2 years)

Downsides

- Growth is slower than inflation in many cases

- Not suitable for long-term wealth building

What investing means in 2025

Investing in 2025 means putting your money into assets that grow over time, such as:

- Stocks & ETFs

- Bonds and Treasury bills

- Real estate or REITs

- Cryptocurrency ETFs (SEC-approved Bitcoin & Ethereum ETFs)

- Fractional investing apps

- Robo-advisors with AI-driven optimization

Key 2025 investing trends

- Low-fee index ETFs remain the safest long-term choice

- AI investment advisors give personalized portfolio suggestions

- More employers offering micro-investing perks

- Sustainable and green investing continuing to rise

Benefits

- High long-term growth potential

- Helps beat inflation

- Compound interest builds generational wealth

Downsides

- Market volatility

- Requires patience

- Returns are not guaranteed

Saving vs investing — when to choose which in 2025 explained (H2 with Focus Keyword)

To make the right financial decisions, you must look at:

- Your timeline

- Your risk tolerance

- Your financial goals

- Your current stability

In 2025, experts generally recommend a hybrid strategy — combining saving and investing — but the proportions depend on your situation. Below is a detailed breakdown.

When to choose saving

Choose saving in 2025 when your goals are short-term, stable, or require immediate liquidity.

1. You don’t have an emergency fund

Financial experts recommend 3–6 months of expenses in liquid savings.

This remains the top priority in 2025 because:

- Inflation still creates price unpredictability

- Health and job markets remain mildly volatile

- Unexpected expenses are more common

2. Your goal is less than 2 years away

You should save, not invest, for goals like:

- Buying a phone, computer, or car

- Wedding or vacation

- Tuition payments

- House down payments within 24 months

3. You cannot afford to lose money

Savings accounts are risk-free. If your financial situation is unstable, saving is safer.

4. You’re preparing for major life changes

If you’re getting married, expecting a child, relocating, or starting a business, saving helps you maintain cushion.

When to choose investing

Choose investing in 2025 when you have long-term goals and a stable financial safety net.

1. Your goal is more than 3 years away

Investing wins when the timeline is long enough to recover from market dips.

Great for:

- Retirement

- Kid’s education fund

- Long-term wealth building

- Buying property in 2028+

2. You already have an emergency cushion

Only invest after forming your emergency fund.

3. You want to beat inflation

Inflation is projected to average 2.6–3.1% in 2025 globally.

Savings rates often fall below this range—investing helps you stay ahead.

4. You want compound growth

Investing compounds your returns and builds long-term wealth. Even modest contributions today can yield significant returns 10–20 years later.

5. You’re comfortable with moderate risk

Investing always carries risk, but diversified ETFs, robo-advisors, and bonds reduce volatility.

Saving vs Investing Comparison Table (2025)

| Feature | Saving | Investing |

|---|---|---|

| Risk | Zero (FDIC insured) | Low to high |

| Best Timeline | 0–2 years | 3+ years |

| Returns | 3–5% APY in 2025 | 6–12% annual (historical) |

| Liquidity | Immediate | Varies |

| Goal Type | Emergency, short term | Growth, long term |

| Tools | Banks, fintech | ETFs, robo-advisors |

| Ideal User | Stability-seekers | Wealth-builders |

Real-Life Examples for 2025

Example 1: Saving is better

A 27-year-old planning to buy a car in early 2026 (in 12 months):

- Goal is short-term

- Market volatility risk is not worth it

- High-yield savings account at ~4% APY is better

Example 2: Investing is better

A 35-year-old planning early retirement at age 55:

- 20-year timeline

- Stock & ETF investing offers compounding

- Robo-advisor portfolio is ideal

Example 3: Hybrid strategy

A family with $10K saved, expecting a child in 2025:

- Keep $6K in savings for emergencies

- Invest $4K in S&P 500 ETF for long-term

- Automate contributions using AI-budgeting apps

Expert Recommendations for 2025

These recommendations align with Forbes, Investopedia, and major financial planners.

1. Build savings first

Always create your emergency fund before investing.

↪ Reference:

Investopedia — Emergency Fund Guide

2. Use AI budgeting apps

2025’s AI apps (Cleo, Copilot, Revolut AI Insights) help automate:

- Spending analysis

- Predictive savings

- Investment suggestions

3. Prioritize index ETFs

Low-fee ETFs such as VTI, VOO, SCHD, and ITOT remain the smartest picks.

↪ Reference:

Forbes — Best ETFs

4. Avoid timing the market

Invest consistently using Dollar-Cost Averaging (DCA).

5. Review your plan every quarter

Use apps or meet a financial advisor yearly.

Common Mistakes to Avoid in 2025

❌ 1. Keeping all money in savings

Inflation reduces long-term value.

❌ 2. Investing without an emergency fund

This is the #1 cause of forced losses when emergencies arise.

❌ 3. Chasing “hot” investments

Viral trends often lead to emotional investing.

❌ 4. Ignoring fees

High fees silently destroy returns.

Choose robo-advisors or ETFs with low expenses (0.03%–0.15%).

❌ 5. Not diversifying

Always spread investments across:

- ETFs

- Bonds

- Real estate

- Cash reserves

❌ 6. Waiting too long to start

In 2025, automation makes investing easier than ever.

The earlier you begin, the more compound interest works for you.

FAQ: Saving vs Investing — When to Choose Which in 2025

1. Is saving better than investing in 2025?

Saving is better for short-term goals and emergencies.

Investing is better for long-term growth.

2. How much should I save before I invest?

Aim for 3–6 months of expenses.

3. Should I invest during economic uncertainty?

Yes, if your timeline is long (5+ years).

Market dips often create better entry points.

4. What are the safest investments in 2025?

- Bond ETFs

- Treasury bills

- Index funds

- Real estate ETFs

5. Are AI robo-advisors reliable in 2025?

Yes — they use modern risk modeling and automate rebalancing.

6. Can I both save and invest?

Absolutely. A hybrid strategy is ideal for most people.

Conclusion: How to Decide Between Saving and Investing in 2025

Choosing between saving and investing in 2025 depends on your:

- Financial stability

- Time horizon

- Risk tolerance

- Personal goals

Save when you need safety and liquidity.

Invest when you want growth and long-term wealth.

A balanced approach — emergency savings + diversified investments — is the smartest strategy this year.

👉 Start by reviewing your goals. Build your emergency fund. Then automate your investments step-by-step. Your future self will thank you.

You can read more about Making Money Online here.