Discover the Best Budgeting Methods for 2025. Learn simple, proven strategies to save more, cut expenses, and take full control of your money as a beginner.

Introduction

The search for the Best Budgeting Methods has become more important than ever in 2025. With rising living costs, digital payments, and changing financial habits, beginners need simple and effective ways to understand and manage their money. The good news is that the Best Budgeting Methods available today are designed specifically for clarity, flexibility, and long-term success, even if you’re starting from zero.

Choosing the Best Budgeting Methods helps you take control of your finances, reduce stress, avoid unnecessary spending, and finally start building savings. Whether your goal is to pay off debt, manage monthly expenses, or grow your financial future, using the right budgeting approach can completely transform how you handle money.

This guide explores the Best Budgeting Methods for beginners in 2025—methods that are practical, beginner-friendly, and proven to work. Each method includes clear explanations, examples, pros and cons, and step-by-step instructions so you can choose the one that fits your lifestyle and financial goals.

By the end of this guide, you’ll understand exactly which of the Best Budgeting Methods works best for you—giving you the confidence to finally take control of your financial life.

The 50/30/20 Rule

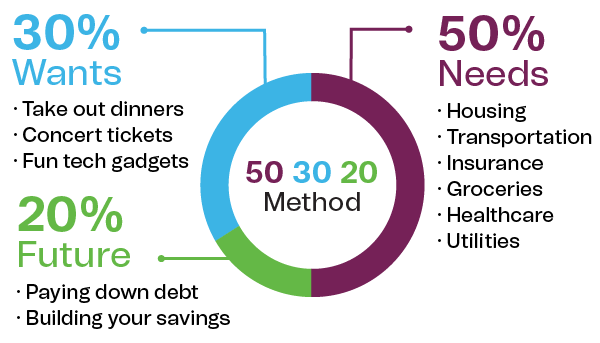

The 50/30/20 Rule remains one of the Best Budgeting Methods for beginners because it offers a clear, balanced, and easy way to manage monthly income. Instead of tracking dozens of categories, this method simplifies your budget into just three spending groups—making it extremely beginner-friendly in 2025.

1. What Is the 50/30/20 Rule?

The 50/30/20 Rule divides your after-tax income into:

- 50% Needs

Essential expenses such as rent, groceries, transportation, utilities, medications, and insurance. - 30% Wants

Non-essential lifestyle choices like entertainment, dining out, shopping, subscriptions, or hobbies. - 20% Savings or Debt

Emergency funds, investments, retirement, sinking funds, or extra debt payoff.

This simplicity is what makes it one of the Best Budgeting Methods for building healthy financial habits.

Pros of the 50/30/20 Rule

- Extremely beginner-friendly

- Easy to maintain long-term

- Provides a balanced approach to spending

- Helps reduce overspending on wants

- Works well for most income levels

Cons of the 50/30/20 Rule

- Not ideal for high cost-of-living areas

- Needs may exceed 50% for some households

- Lacks detailed tracking for precise budgeting

- May feel too broad for people wanting tight control

Example Breakdown

If your take-home pay is $3,000 per month, your budget might look like:

- $1,500 (50%) — Needs

- $900 (30%) — Wants

- $600 (20%) — Savings or Debt Payments

This layout helps beginners instantly understand where their money goes, reinforcing why this is one of the Best Budgeting Methods for simplicity and balance.

How to Use the 50/30/20 Rule (Step-by-Step)

Step 1: Calculate Your After-Tax Income

Use your paycheck amount after taxes and deductions.

Step 2: Separate Needs From Wants

This is the most important step—identify essentials vs. extras.

Step 3: Assign Percentages to Each Category

Aim for the 50/30/20 ratio as closely as possible.

Step 4: Adjust Gradually

If needs exceed 50%, reduce wants or slowly improve spending patterns.

Step 5: Track Monthly Progress

Use tools like Mint, YNAB, or a simple spreadsheet.

Why This Is One of the Best Budgeting Methods

The 50/30/20 Rule continues to be ranked among the Best Budgeting Methods because it teaches beginners balance, control, and awareness without requiring strict tracking or complicated systems. It’s flexible, stress-free, and easy to stick to—making it the perfect starting point for anyone new to budgeting in 2025.

Zero-Based Budgeting

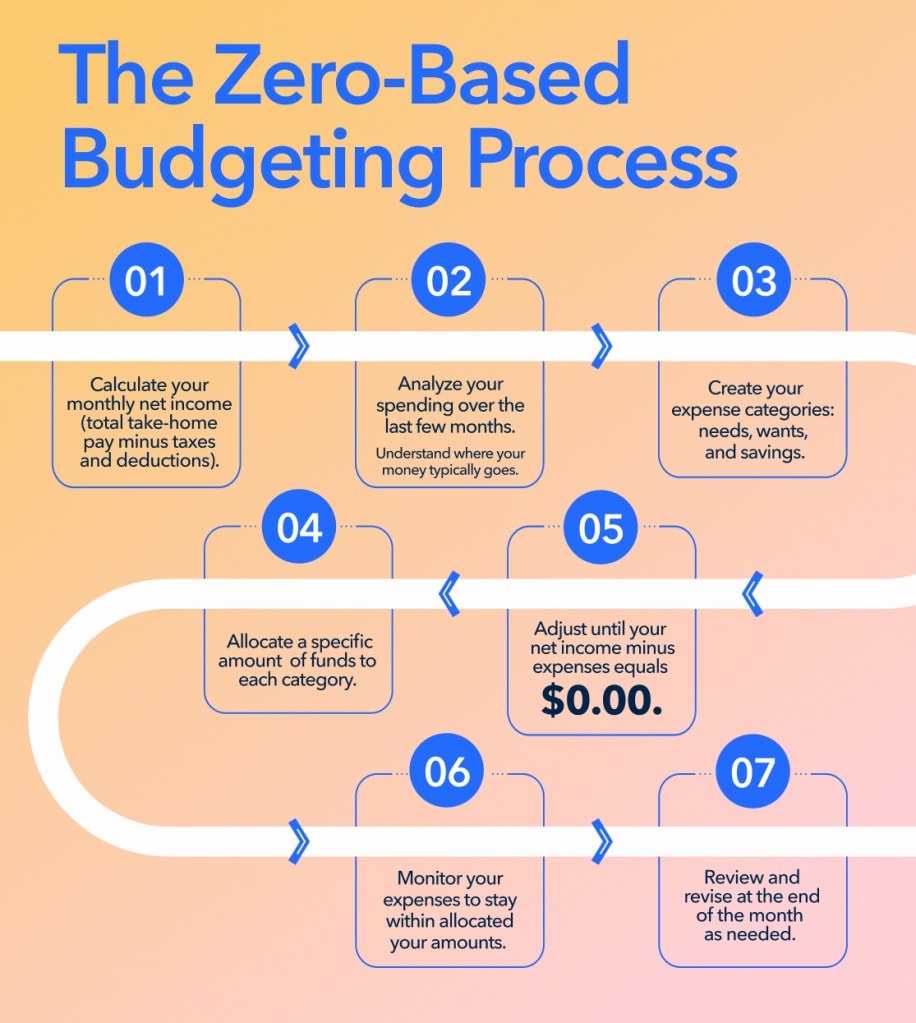

Zero-Based Budgeting is one of the Best Budgeting Methods for beginners who want maximum clarity and control. Unlike traditional budgeting, where you estimate spending loosely, Zero-Based Budgeting assigns every single dollar a purpose. By the end of the month, your income minus your expenses should equal zero — not because you’re broke, but because every dollar is allocated intentionally.

This method is especially powerful for beginners who overspend or feel unsure about where their money goes.

2. What Is Zero-Based Budgeting?

Zero-Based Budgeting means creating a plan where:

👉 Every dollar has a job

👉 No money is left unassigned

👉 You decide exactly where each dollar goes

Your monthly income is divided into categories such as:

- Rent

- Groceries

- Utilities

- Debt payments

- Savings

- Investments

- Subscriptions

- Transportation

- Entertainment

This intentional level of detail is why it’s considered one of the Best Budgeting Methods for beginners who want structure and accountability.

Pros of Zero-Based Budgeting

- Complete clarity on where every dollar goes

- Helps reduce unnecessary spending

- Encourages mindful financial decisions

- Excellent for paying off debt faster

- Ideal for people who often lose track of money

Cons of Zero-Based Budgeting

- Can be time-consuming for beginners

- Requires regular tracking and adjustments

- Might feel restrictive for flexible spenders

- Harder to maintain with irregular income

Example Breakdown

If your monthly take-home income is $3,000, a Zero-Based Budget might look like:

- Rent: $1,200

- Groceries: $350

- Utilities: $150

- Transportation: $200

- Phone/Internet: $100

- Insurance: $160

- Entertainment: $150

- Restaurants: $140

- Emergency Savings: $300

- Investments: $150

- Debt Repayment: $100

Total = $3,000 → Every dollar assigned → Zero remaining.

This precision is what makes it one of the Best Budgeting Methods for beginners who want control and awareness.

How to Use Zero-Based Budgeting (Step-by-Step)

Step 1: Calculate Your Monthly Income

Include salary, side earnings, freelance income, or financial support.

Step 2: List Every Expense Category

Don’t skip anything — even small categories like apps or parking.

Step 3: Assign a Dollar Amount to Each Category

Adjust until your income minus expenses equals zero.

Step 4: Track Your Spending Weekly

Use apps like YNAB, EveryDollar, or spreadsheets.

Step 5: Review and Improve Each Month

Your budget gets more accurate with practice.

Why This Is One of the Best Budgeting Methods

Zero-Based Budgeting stands out among the Best Budgeting Methods because it forces clarity. Beginners quickly understand their spending patterns and learn to control their money intentionally. It also supports better savings, debt reduction, and long-term financial discipline — making it one of the top budgeting strategies in 2025.

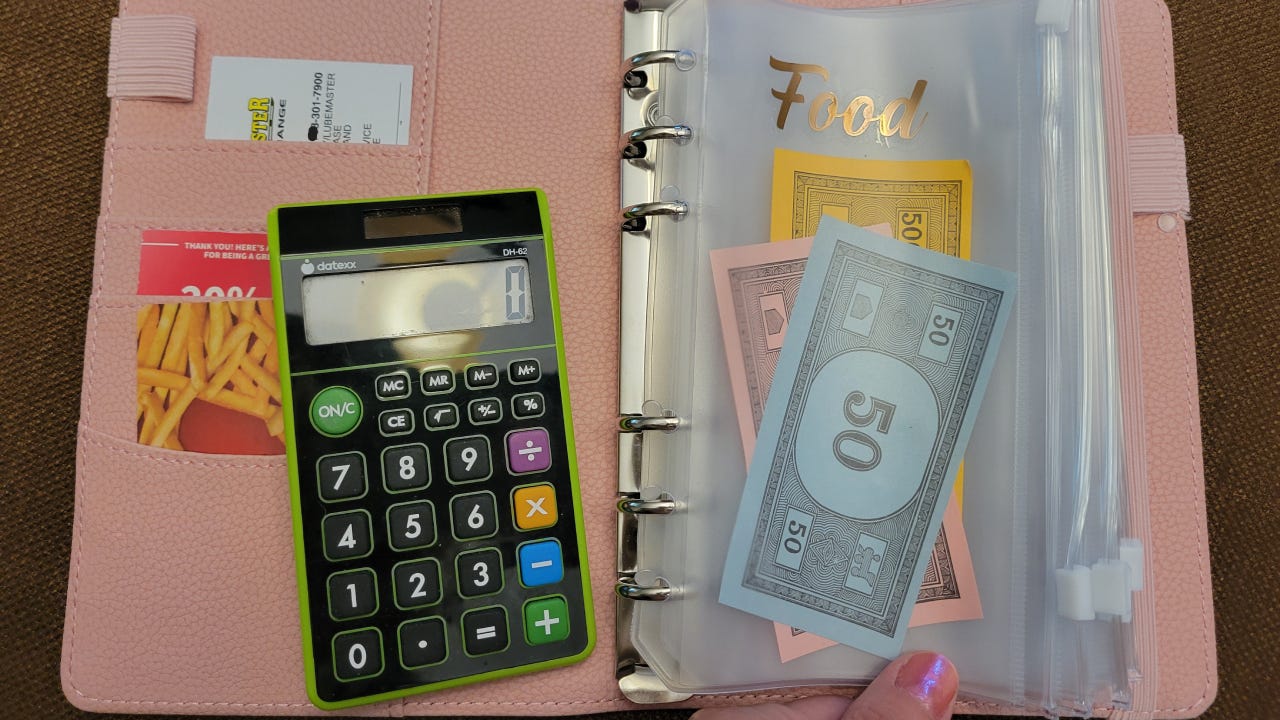

Envelope / Cash Stuffing System

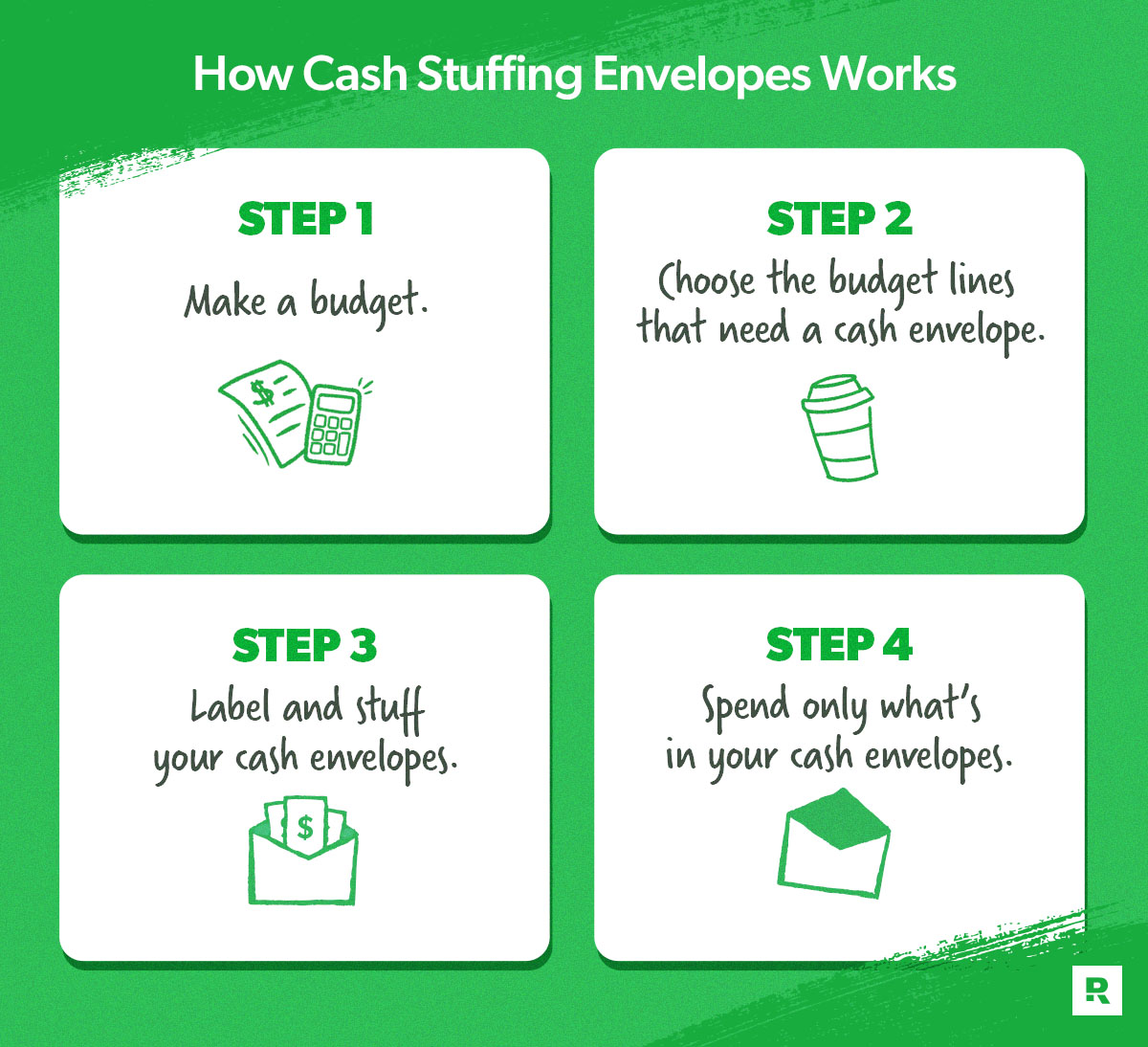

The Envelope Budgeting Method, also known as the Cash Stuffing System, is one of the Best Budgeting Methods for beginners who struggle with overspending. This system uses physical envelopes (or digital versions) to assign cash to specific spending categories. Once an envelope is empty, spending in that category stops—making this one of the most powerful methods for financial discipline.

In 2025, this method remains popular thanks to TikTok “cash stuffing” trends and the rise of digital envelope apps.

3. What Is the Envelope Budgeting Method?

The Envelope Method divides your monthly spending into categories and assigns a set amount of cash to each. Common envelope categories include:

- Groceries

- Gas/Transportation

- Dining Out

- Shopping

- Entertainment

- Personal Care

- Household Items

Each envelope holds the exact amount of money budgeted for the month. When the envelope is empty, you can’t spend more. This built-in restriction is what makes the Envelope Method one of the Best Budgeting Methods for controlling impulsive spending.

Pros of the Envelope System

- Perfect for beginners who overspend

- Encourages mindful, disciplined spending

- Easy to see remaining money visually

- Eliminates hidden or forgotten expenses

- Doesn’t require complex apps or tools

Cons of the Envelope System

- Requires withdrawing and carrying cash

- Inconvenient for online purchases or bills

- Can feel old-fashioned in a digital world

- May be unsafe to carry large amounts of money

- Strict limits may feel too rigid for some

Example Breakdown

Let’s say you budget $900 for variable expenses:

- Groceries: $300

- Gas: $150

- Dining Out: $150

- Entertainment: $100

- Shopping: $200

You place the exact amount in each envelope. If your dining-out envelope hits zero on the 20th of the month, you stop dining out or move money from another envelope (not recommended if you want strong discipline).

This simplicity is why it’s still one of the Best Budgeting Methods for beginners learning spending control.

How to Use the Envelope System (Step-by-Step)

Step 1: Choose Spending Categories

Pick areas where you tend to overspend—usually 5–10 categories.

Step 2: Set Monthly Limits for Each Envelope

Look at past bank statements for realistic numbers.

Step 3: Withdraw Cash for All Envelopes

Use exact amounts so you don’t mix categories.

Step 4: Spend Only From the Correct Envelope

Don’t mix envelopes. When it’s empty, stop spending.

Step 5: Track Leftover Cash Monthly

Roll it over, save it, or apply it to debt.

Bonus (2025 Trend): Use Digital Envelopes

Apps like Goodbudget, Mvelopes, and Qube Money offer modern versions of this method using cards instead of cash.

Why This Is One of the Best Budgeting Methods

The Envelope Method is one of the Best Budgeting Methods because it creates instant spending awareness. When beginners physically see money leaving their hands—or see their digital “envelopes” empty—they naturally become more intentional with their purchases. It builds discipline, prevents overspending, and helps beginners understand real spending patterns quickly.

4. Pay-Yourself-First Budgeting

(Alt text: Best Budgeting Methods – Pay Yourself First Budgeting)

The Pay-Yourself-First Budgeting Method is one of the Best Budgeting Methods for beginners who want to build savings automatically. Instead of saving whatever is left at the end of the month, this method prioritizes saving first — before paying bills, before spending, and before anything else.

By making saving the top priority, beginners quickly develop strong financial habits and build long-term security without overthinking the process.

What Is Pay-Yourself-First Budgeting?

Pay-Yourself-First means setting aside a fixed portion of your income immediately when you get paid. This can include:

- Emergency savings

- Retirement contributions

- Investments

- Sinking funds

- Major purchase savings

- Extra debt payoff

Whatever remains after saving is used for needs and wants. This ‘savings-first’ approach is why it’s considered one of the Best Budgeting Methods for financial growth.

Pros of Pay-Yourself-First Budgeting

- Builds savings automatically

- Helps beginners grow wealth without feeling restricted

- Reduces stress by focusing on financial security

- Works well with any income level

- Creates consistency and builds long-term discipline

Cons of Pay-Yourself-First Budgeting

- Requires planning to handle remaining income

- May feel restrictive for people living paycheck to paycheck

- Not ideal for highly irregular income unless carefully adjusted

Example Breakdown

If your monthly take-home pay is $3,000, your Pay-Yourself-First plan might look like:

- $500 → Savings

- $200 → Investments

- $200 → Debt repayment

- Remaining $2,100 → Bills, needs, and wants

By focusing on savings first, beginners quickly build financial stability, making this one of the Best Budgeting Methods in 2025.

How to Use the Pay-Yourself-First Method (Step-by-Step)

Step 1: Decide How Much You Want to Save Monthly

Beginners typically start with 10–20% of income.

Step 2: Automate the Transfers

Schedule automatic deposits on payday to:

- High-yield savings

- Investment accounts

- Retirement funds

- Sinking funds

Step 3: Pay Bills After Saving

Cover essentials next: rent, utilities, groceries, insurance.

Step 4: Use Remaining Money for Wants

Dining out, entertainment, subscriptions, etc.

Step 5: Review Your Savings Rate Every 3–6 Months

Increase savings as income rises or expenses decrease.

Why This Is One of the Best Budgeting Methods

The Pay-Yourself-First approach is one of the Best Budgeting Methods because it creates a strong financial foundation automatically. By saving before spending, beginners stay consistent, reduce stress, and build wealth steadily. It minimizes emotional or impulsive spending and ensures money moves toward long-term goals every single month.

5. Reverse Budgeting

Reverse Budgeting is one of the Best Budgeting Methods for beginners who want to put their goals first—not their expenses. Instead of starting with bills and daily spending, this method begins by deciding how much money you want to save or invest each month. Only after your goals are covered do you budget the remaining amount for living expenses.

This goal-first approach is perfect for the 2025 beginner who wants direction, structure, and long-term financial progress.

What Is Reverse Budgeting?

Reverse Budgeting shifts the focus from “spend first, save later” to:

👉 Save first. Spend later.

You identify your top financial priorities and allocate money to them immediately. These may include:

- Emergency fund

- Retirement contributions

- Investing

- Debt repayment

- Home down payment

- Travel fund

- Big purchases (laptop, furniture, car)

Once these goals are funded, the rest of your income is used for everyday expenses. This clarity is what makes Reverse Budgeting one of the Best Budgeting Methods for people who want to build wealth intentionally.

Pros of Reverse Budgeting

- Highly goal-focused and structured

- Helps beginners build wealth faster

- Reduces emotional or impulsive spending

- Perfect for long-term planning

- Works well alongside other Best Budgeting Methods

Cons of Reverse Budgeting

- May require adjusting lifestyle spending

- Harder for people with unpredictable income

- Requires discipline to limit non-essential spending

- Needs regular review to stay aligned with changing goals

Example Breakdown

If your monthly income is $3,000, your Reverse Budget might look like:

- $300 → Emergency fund

- $200 → Retirement

- $150 → Investing

- $200 → Debt repayment

Total saved first: $850

You then use the remaining $2,150 for:

- Rent

- Groceries

- Utilities

- Transportation

- Entertainment

- Subscriptions

This ensures that long-term goals are never ignored—one of the biggest reasons it’s considered one of the Best Budgeting Methods in 2025.

How to Use Reverse Budgeting (Step-by-Step)

Step 1: Identify Your Top Financial Goals

Choose 3–5 clear goals such as savings, investments, or debt elimination.

Step 2: Assign a Monthly Goal Amount

Use calculators to determine how much you need to contribute.

Step 3: Automate Your Goal Contributions

Set up automatic transfers on payday.

Step 4: Use Remaining Money for Expenses

Cover essentials like housing, food, bills, and transportation.

Step 5: Review Every 6 Months

As your income grows, increase your contributions to speed up progress.

Why This Is One of the Best Budgeting Methods

Reverse Budgeting is one of the Best Budgeting Methods because it creates intentional progress. Instead of hoping to save whatever is left over, you guarantee savings first. This method ensures you’re always moving toward your biggest financial goals—making it one of the top budgeting strategies for beginners in 2025.

6. Line-Item Budgeting

Line-Item Budgeting is one of the Best Budgeting Methods for beginners who want extreme clarity and detail. Instead of grouping expenses into broad categories, this method breaks down your budget into specific, individual cost items. Every dollar has a label, every spending category is precise, and nothing is left vague.

This makes Line-Item Budgeting ideal for beginners who want accuracy, transparency, and full financial control.

What Is Line-Item Budgeting?

Line-Item Budgeting means you create a detailed budget where each expense is listed individually. Instead of “groceries,” you may list categories like:

- Fruits & vegetables

- Household supplies

- Cleaning products

- Meat & dairy

Instead of “transportation,” you might list:

- Gas

- Public transit

- Car maintenance

- Parking fees

This level of detail makes Line-Item one of the Best Budgeting Methods for people who want to track exactly where their money goes.

Pros of Line-Item Budgeting

- Provides crystal-clear spending awareness

- Helps identify unnecessary or hidden expenses

- Very effective for eliminating wasteful spending

- Great for detail-oriented beginners

- Works well for households with variable expenses

Cons of Line-Item Budgeting

- Time-consuming to set up and maintain

- May feel overwhelming for complete beginners

- Harder to use with fluctuating incomes

- Requires precise tracking throughout the month

Example Breakdown

For a monthly take-home income of $3,000, your Line-Item Budget might look like:

- Rent: $1,200

- Groceries:

- $140 meat

- $60 vegetables

- $40 snacks

- $50 household items

- Utilities: $150

- Subscriptions:

- $15 Spotify

- $20 Netflix

- $10 iCloud

- Phone: $40

- Gas: $120

- Eating Out: $100

- Shopping: $120

- Savings: $300

- Investments: $150

- Emergency Fund: $150

This level of visibility is what makes it one of the Best Budgeting Methods for accurate financial planning.

How to Use Line-Item Budgeting (Step-by-Step)

Step 1: Track Your Spending for 30 Days

Examine past transactions to identify your real spending categories.

Step 2: Create Detailed Line Items

Break broad categories into smaller, more precise ones.

Step 3: Assign an Amount to Each Line Item

Use past spending data for accuracy.

Step 4: Track Every Purchase

Log all expenses daily or weekly to stay updated.

Step 5: Review What You Can Reduce

Cut wasteful categories and reassign money to savings or debt.

Why This Is One of the Best Budgeting Methods

Line-Item Budgeting earns its place among the Best Budgeting Methods because of its precision. Beginners quickly understand their true spending habits and identify areas for improvement. This method works exceptionally well for people who want full control of their finances and a clear financial picture every month.

7. The Calendar Budget Method

(Alt text: Best Budgeting Methods – Calendar Budget Method)

The Calendar Budget Method is one of the Best Budgeting Methods for beginners who want a simple way to visualize their cash flow. Instead of only looking at monthly totals, this method helps you see when money comes in and when bills are due. For beginners in 2025—especially those with irregular income or many due dates—this method brings structure and prevents financial surprises.

What Is the Calendar Budget Method?

The Calendar Budget Method uses a calendar (digital or paper) to map out:

- Payday dates

- Bill due dates

- Subscription renewals

- Weekly expenses (groceries, gas)

- Savings or investment transfers

By placing all financial activity onto a monthly calendar, beginners can predict cash flow more easily and avoid late fees or overdrafts. This time-based clarity makes it one of the Best Budgeting Methods for visual thinkers.

Pros of the Calendar Budget Method

- Excellent for irregular or variable income

- Helps avoid late fees and missed payments

- Provides a visual understanding of cash flow

- Reduces the stress of unexpected bills

- Works well alongside other Best Budgeting Methods

Cons of the Calendar Budget Method

- Requires regular updates

- Less helpful for long-term saving goals

- Can get crowded if you list too many small expenses

- Not ideal for people who dislike tracking dates

Example Breakdown

Imagine your monthly income is $3,000, paid on the 1st and 15th.

Your calendar might look like this:

- 1st: Paycheck

- 3rd: Car insurance ($90)

- 5th: Rent ($1,200)

- 10th: Utilities ($150)

- 15th: Paycheck

- 17th: Subscriptions (Netflix, Spotify, iCloud – $45 total)

- 22nd: Groceries (weekly $80–$100)

- 24th: Gas ($40)

By seeing exact dates, you can prevent overspending before major bills. This timing-based structure makes it one of the Best Budgeting Methods for staying organized and prepared.

How to Use the Calendar Budget Method (Step-by-Step)

Step 1: Write Down All Paydays

Mark your income dates first.

Step 2: Add All Recurring Bills

Rent, utilities, subscriptions, insurance, debt payments.

Step 3: Include Weekly or Flexible Expenses

Groceries, gas, childcare, medicine, etc.

Step 4: Schedule Savings Transfers

Pick dates for automatic savings—even small amounts.

Step 5: Review Weekly

Adjust as new expenses come up or due dates shift.

Why This Is One of the Best Budgeting Methods

The Calendar Budget Method earns its place among the Best Budgeting Methods because it removes guesswork. Beginners get a clear, visual plan that shows when money arrives and when it needs to go out. It reduces stress, improves cash flow management, and helps prevent both overspending and overdue bills—making it especially valuable in 2025’s fast-paced financial environment.

Comparison Table

Choosing among the Best Budgeting Methods can feel overwhelming, especially for beginners. This comparison table gives you a clear, simple overview so you can quickly identify which method fits your lifestyle, goals, and financial habits.

Below is a side-by-side comparison of all seven Best Budgeting Methods featured in this guide:

Comparison of the Best Budgeting Methods

| Budgeting Method | Best For | Difficulty Level | Flexibility | Ideal For Beginners? | Automation |

|---|---|---|---|---|---|

| 50/30/20 Rule | Balanced, simple budgeting | Easy | High | Yes | Medium |

| Zero-Based Budgeting | Full control & detailed tracking | Medium–Hard | Low | Yes, with discipline | Low |

| Envelope / Cash Stuffing | Overspenders & visual learners | Medium | Low | Yes | None (unless using digital envelopes) |

| Pay-Yourself-First | Savings & wealth-building | Easy | High | Yes | High (automated transfers) |

| Reverse Budgeting | Goal-focused savers | Easy | Medium | Yes | Medium |

| Line-Item Budgeting | Detailed expenses & accuracy | Hard | Medium | Not ideal for absolute beginners | Low |

| Calendar Budget Method | Cash flow management & bill timing | Easy–Medium | High | Yes | Medium |

How to Use This Comparison Table

- If you want simplicity, choose 50/30/20.

- If you need strict control, choose Zero-Based Budgeting.

- If you overspend, pick the Envelope Method.

- If your goal is savings, choose Pay-Yourself-First or Reverse Budgeting.

- If you love details, go for Line-Item Budgeting.

- If you want a visual timeline, use the Calendar Method.

Each of these approaches is one of the Best Budgeting Methods depending on your personality, income type, and financial goals.

Conclusion

Choosing the Best Budgeting Methods in 2025 doesn’t need to feel overwhelming. Each method you explored in this guide offers a unique approach to managing your money, whether you want simplicity, precision, discipline, or long-term financial growth. The key is not to find a “perfect” method—it’s to choose the method that feels realistic, comfortable, and doable for your lifestyle.

From the straightforward 50/30/20 Rule to the highly structured Zero-Based Budgeting, the visual clarity of the Envelope System, or the long-term power of Pay-Yourself-First and Reverse Budgeting, every method here has the potential to transform your financial habits. Even highly detailed systems like Line-Item Budgeting and visual tools like the Calendar Budget Method play an important role in helping beginners understand and organize their financial lives.

The Best Budgeting Methods work because they give you structure, clarity, and confidence. You don’t need to master all seven—just choose the one that matches your personality and goals. As long as you remain consistent and intentional, your finances will get stronger month by month.

Your journey to better money management starts with a single step: picking one budgeting method and applying it today. The right system will help you save more, spend smarter, and build a stable financial future in 2025 and beyond.

Frequently Asked Questions (FAQ)

1. What are the Best Budgeting Methods for complete beginners?

The Best Budgeting Methods for complete beginners are the 50/30/20 Rule and the Pay-Yourself-First Method. These offer structure without adding complexity. For beginners wanting a deeper explanation of the 50/30/20 Rule, this guide from Investopedia is helpful: https://www.investopedia.com/50-30-20-rule-4769835

2. Can I combine multiple Best Budgeting Methods at once?

Yes, combining the Best Budgeting Methods is not only possible but often highly effective. For example, you can use Pay-Yourself-First for savings while applying digital envelopes for spending categories. To explore how digital envelope budgeting works, check this NerdWallet resource: https://www.nerdwallet.com/article/finance/cash-envelope-system

3. How long does it take to see results from budgeting?

Most people notice improvements within the first 30 days. You’ll gain clarity about spending patterns and reduce overspending quickly. Financial transformation—like building emergency savings or reducing debt—typically becomes more visible within 3–6 months. For additional budgeting insights, see the Consumer.gov budgeting guide: https://www.consumer.gov/articles/1002-making-budget

4. Which budgeting method is best for irregular income?

For irregular income, the Calendar Budget Method and Zero-Based Budgeting work extremely well. They help you manage cash flow and ensure every dollar has a purpose. For a detailed look at Zero-Based Budgeting, refer to this Investopedia article: https://www.investopedia.com/zero-based-budgeting-4769822

5. What if I keep failing at budgeting every month?

If you’re struggling to stick with a budget, start with simpler Best Budgeting Methods such as the 50/30/20 Rule or Pay-Yourself-First. These methods reduce stress and help you build consistency gradually. For more guidance on fixing budgeting mistakes, this NerdWallet breakdown can help: https://www.nerdwallet.com/article/finance/budgeting-mistakes

6. Do I need budgeting apps to use the Best Budgeting Methods?

No, budgeting apps are optional. You can use the Best Budgeting Methods with notebooks, spreadsheets, or printable templates. However, many beginners find apps like Mint, YNAB, and Rocket Money helpful for automation. To compare popular budgeting apps, refer to this NerdWallet comparison: https://www.nerdwallet.com/best/finance/budgeting-apps

Call-to-Action

Call-to-Action

You’ve now explored the Best Budgeting Methods for beginners in 2025—from simple systems like the 50/30/20 Rule to more intentional frameworks like Reverse Budgeting and Zero-Based Budgeting. The next step is choosing the method that feels realistic, starting small, and staying consistent. Real financial transformation begins with one committed decision.

If you’re ready to take the next step in your financial journey, choose one of the Best Budgeting Methods from this guide and put it into action this week. Start with small, manageable changes, and watch your financial confidence grow month by month.

👉 Want to continue building your money skills?

Check out our Investing Basics section for your next step in financial growth:

https://moneybasicshub.com/category/investing-basics/

This internal resource will help you understand the fundamentals of investing, long-term wealth building, and how to make your money work for you—perfect for beginners who just mastered budgeting.